Overproduction, collapsing BO-HO spreads, and saturated D4 RIN markets complicate the near-term outlook, though new policy-driven incentives are set to take effect in 2025

The Road Ahead: Renewable Diesel and SAF

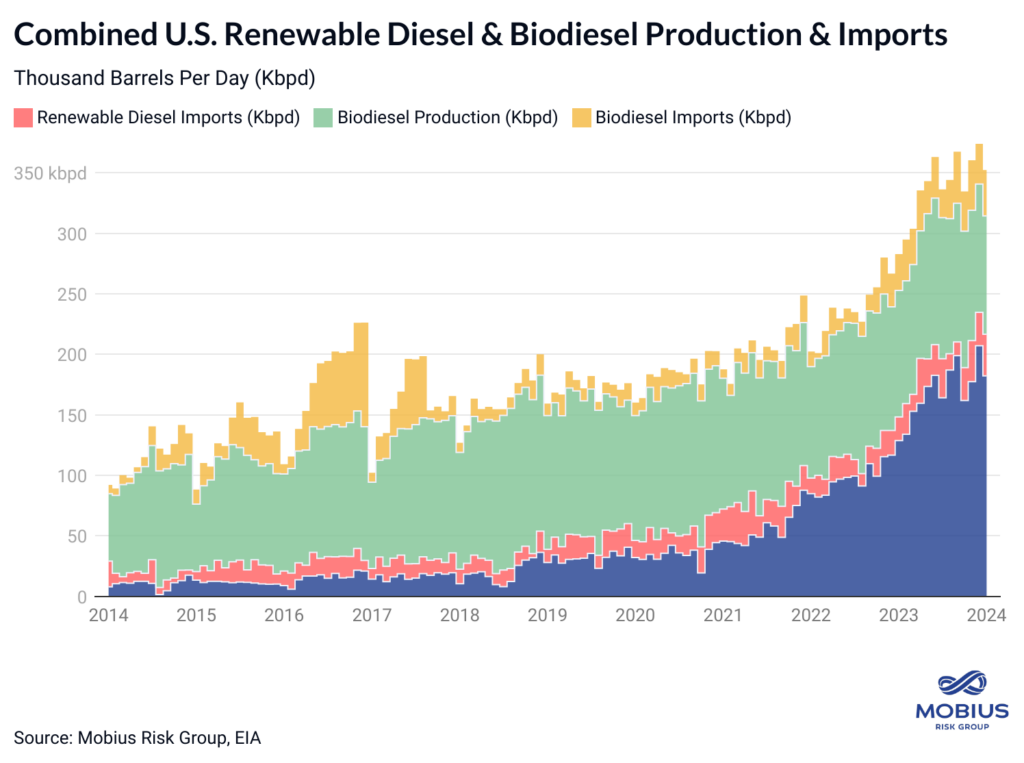

A wave of federal incentives and favorable bean oil spreads brought renewable diesel and sustainable aviation fuel (SAF) producers to the table, vying to capture tax credits and D4 (biomass-based diesel) RINs in combined excess of $2.50/gallon. However, through 2023 and early 2024, these incentives created a new problem: overproduction.

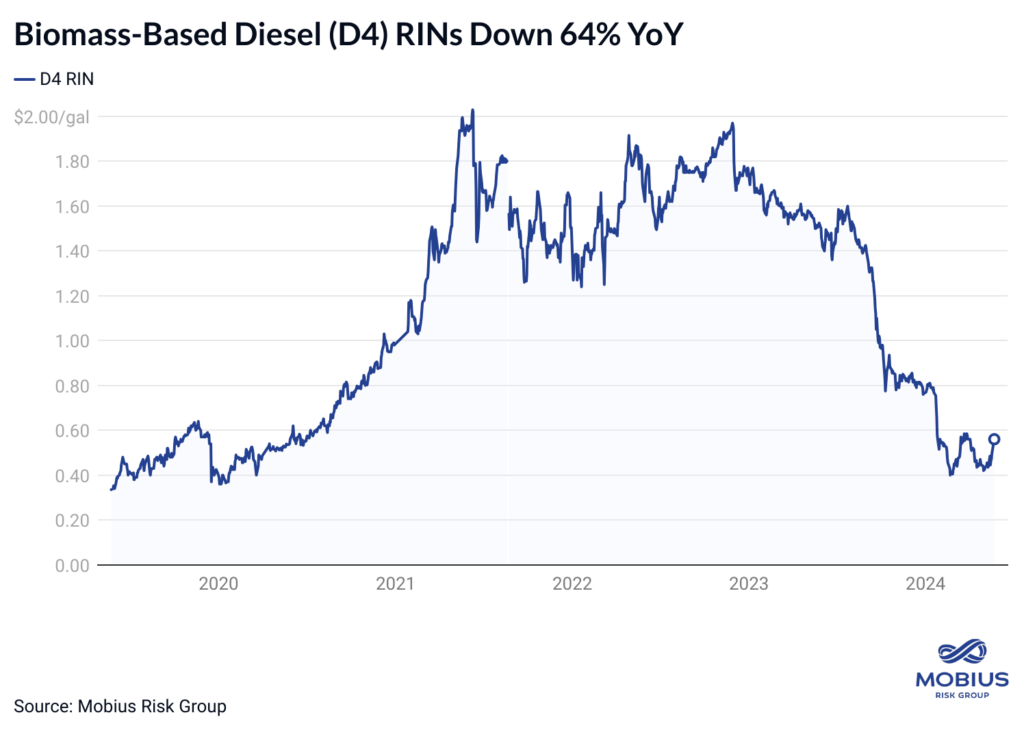

D4 (biomass-based diesel) RINs have plummeted ~64% YoY and over 70% since January 2023 as overproduction depresses the U.S. market for biodiesel, renewable diesel, and sustainable aviation fuel (SAF) compliance credits.

What are RINs?

RINs (Renewable Identification Numbers) are tradable compliance credits under the EPA’s Renewable Fuel Standard (RFS) program. Under this program, the EPA sets annual renewable volume obligations (RVOs) for the minimum volume of biofuels in the U.S. fuel supply.

Renewable diesel and biodiesel production and imports generate D4 RINs, which satisfy biomass-based diesel (D4), advanced biofuel (D5), and total biofuel (D6) RVOs. One gallon of ethanol generates 1.0 RINs, one gallon of biodiesel generates 1.5 RINs, and one gallon of renewable diesel generates either 1.6 or 1.7 RINs, depending on its fuel pathway.

RINs, RVOs, and Capped Growth

Despite the collapse in D4 RINs, producers must also contend with inflexible RVOs, which are not growing quickly enough to accommodate new supply.

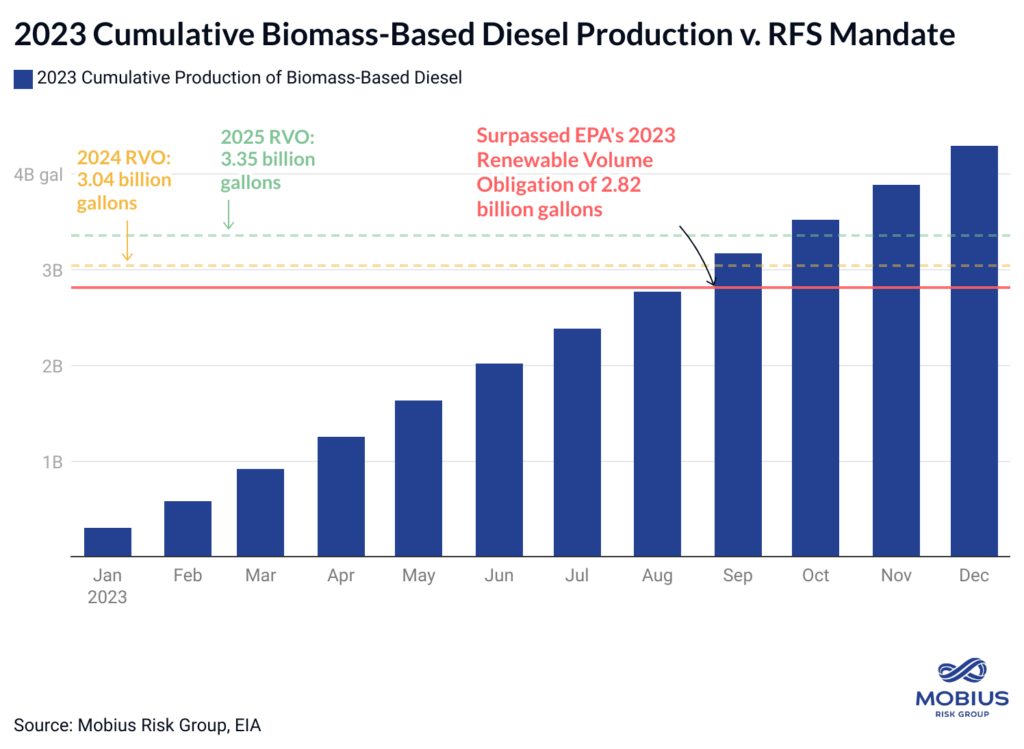

U.S. biomass-based diesel production surpassed the EPA’s 2023 RVO of 2.82 billion gallons by September.

If held at 2023 levels, U.S. production would surpass the EPA’s 2024 and 2025 RVOs by October, offering little relief to D4 RINs in the near-term outlook.

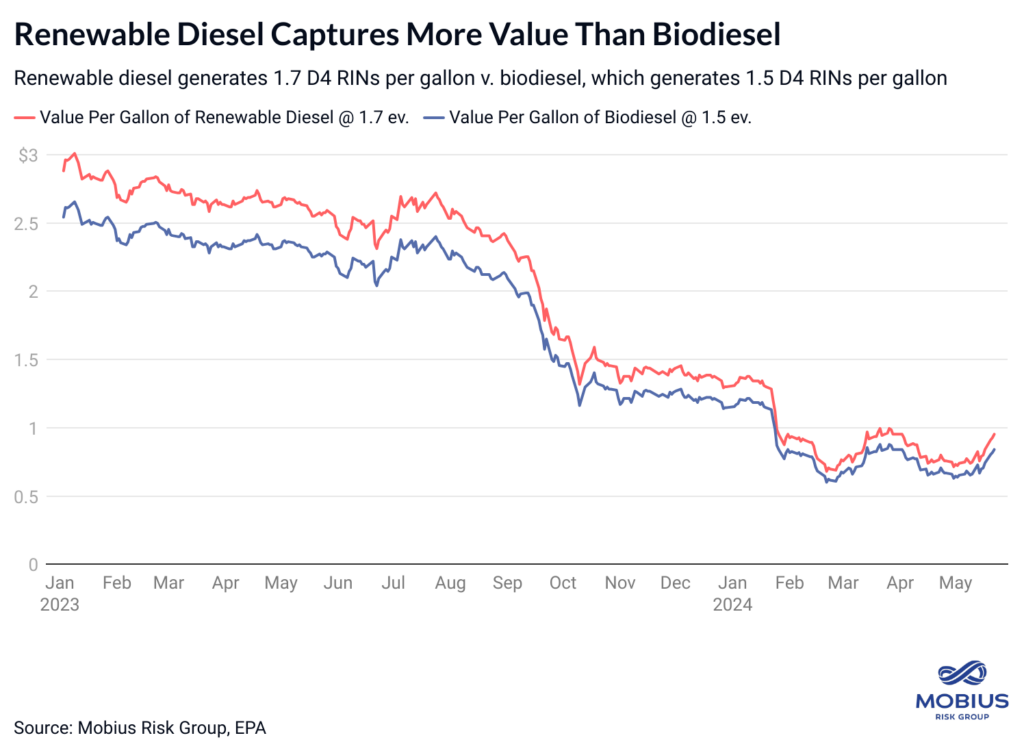

Still, EPA RVOs incentivize producers to expand renewable diesel capacity over biodiesel capacity.

Renewable diesel is a “drop-in” fuel, meaning it can replace petroleum-derived diesel without blending. Biodiesel, meanwhile, must be blended with petroleum diesel for use in standard engines without modifications.

Accordingly, each gallon of renewable diesel generates 1.7 D4 RINs versus 1.5 D4 RINs for each gallon of biodiesel, adding incremental upside to renewable diesel portfolios.

BO-HO Spreads Support Margins

The BO-HO spread represents the difference between the price of soybean oil (the primary feedstock for biodiesel and renewable diesel) and heating oil.

BO-HO spreads have declined over 66% from 2023 highs, as soybean oil prices dropped on robust 2024 crop expectations and heating oil prices jumped on geopolitical risks in the Middle East and Russia.

While lower feedstock costs have buoyed margins during the collapse in D4 RINs, ongoing downside pressure on blending credits and easing HO prices will likely force small producers to trim output accordingly. Large producers, however, are using collapsed D4 RINs as an opportunity to capture market share ahead of next year’s Clean Fuel Production Tax Credit.

New Credit Schemes Geared Towards Renewable Diesel and Sustainable Aviation Fuel

Existing tax credits, such as the Blender’s Tax Credit (BTC) and California’s Low Carbon Fuel Standard Credit, provide credits for imported and domestically-produced biomass-based diesel.

As a result, domestic producers face more competition and prolonged periods of oversupply with more imported volumes in the U.S. market.

Starting in January 2025, however, the Inflation Reduction Act’s Clean Fuel Production Tax Credit will replace the BTC and remove credits for imported fuels.

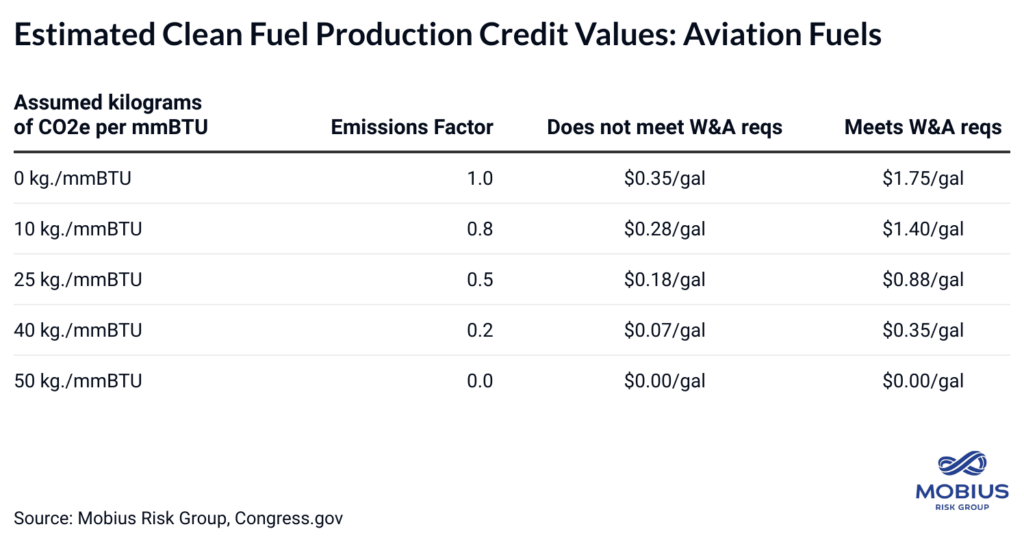

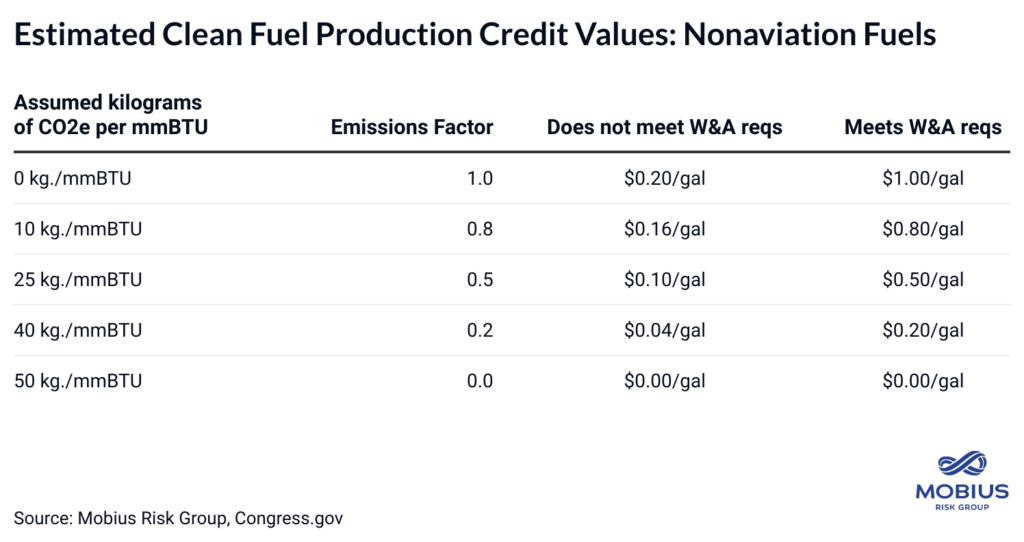

Through the Clean Fuel Production Tax Credit, producers who meet wage and apprenticeship requirements can receive a maximum credit of $1.00 per gallon of non-aviation fuel and $1.75 per gallon of aviation fuel, issued on a sliding scale according to the fuel’s emissions factor relative to 50 kg CO2e per mmBTU.

The more favorable tax credit for aviation fuels has spurred large producers to retool facilities for sustainable aviation fuel production alongside renewable diesel.

Phillips 66, for example, announced in April that its San Francisco Rodeo Renewable Energy Complex has expanded renewable diesel and SAF production to 30,000 bpd and is on course to produce 50,000 bpd by the end of 2Q24, making it one of the world’s largest renewable diesel facilities.

Similarly, Diamond Green Diesel (the joint venture between Darling Ingredients and Valero) announced a final investment decision last year to upgrade 50% of its Port Arthur plant to produce 235 million gallons per year (15.3 kbpd) of SAF.

The Road Ahead:

Renewable diesel producers who can outlast collapsed D4 RINs will be well-positioned to take advantage of Clean Fuel Production Tax Credits in 2025.

Still, biofuels rely on policy-driven adoption, meaning producers are constrained to using RVOs and tax incentives to capture market share from petroleum products.

As we’ve observed with ethanol producers and the D4 RIN market, overproduction beyond these federal targets remains the primary risk factor for renewable fuel stakeholders.

In the crude complex, meanwhile, regulatory and financial barriers to traditional energy investments remain a potent risk factor for volatility and energy price inflation, as petroleum diesel meets more than 12x as much demand as biomass-based diesel at less than 20% of the cost.

If you’d like to receive the downloads associated with this report, please email energyshots@mobiusriskgroup.com