Rystad

Nagorno-Karabakh’s close proximity to key Azeri oil and gas infrastructure means that there will be more at stake if the region’s conflict with Armenia escalates further and jeopardizes key export pipelines. A Rystad Energy analysis explains how potential disruptions could benefit Russian gas exports while weakening both Turkey’s cheap gas imports and its role as a vital oil transport hub.

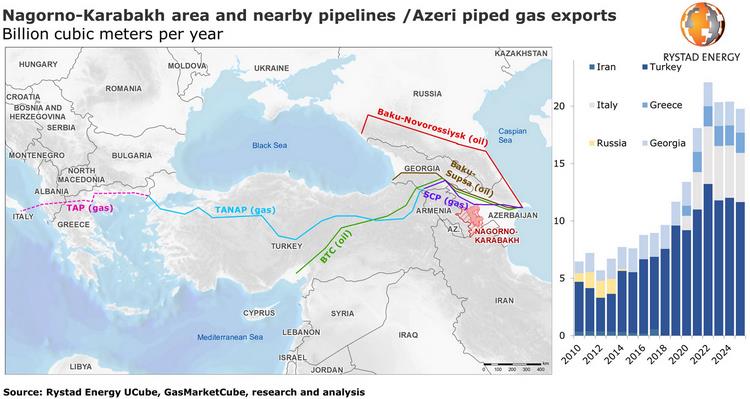

The Baku-Tbilisi-Ceyhan (BTC) oil pipeline and the South Caucasus Pipeline (SCP) gas conduit both run through Azerbaijan, with some sections lying as little as 25 miles from renewed fighting in Nagorno-Karabakh.

Any attack on or seizure of pipeline territory could have serious ramifications for upstream operations in Azerbaijan, and particularly impactful would be any disruption to the giant Azeri-Chirag-Gunashli (ACG) project in the Caspian Sea. These fields, operated by BP, produce about 485,000 bpd of light oil, representing approx. 75% of Azeri crude production. Most of the oil from these fields is exported via the BTC pipeline which, despite its nameplate capacity of 1.2 million bpd, has been operating at half capacity.

The South Caucasus Pipeline carries gas from the Shah Deniz field in the Azeri sector of the Caspian Sea to the Turkish border, where it links with the Trans-Anatolian gas pipeline (TANAP) that runs through Turkey. TANAP, having commenced operations in 2018, will in turn link up with the new Trans Adriatic Pipeline (TAP), thus enabling Azeri gas exports to flow to southeastern Europe. TAP is more than 95% complete, with first deliveries scheduled by year-end, but this project could be jeopardized by the conflict in Nagorno-Karabakh.

‘The pipelines are laid two meters underground, so there is protection there from material damage. However, while it is still too early to forecast possible production disruptions at the offshore ACG and Shah Deniz fields, any scenario where Armenian forces manage to take over territory traversed by export pipelines represents a potential threat to oil and gas exports in the region,’ says Rystad Energy’s upstream analyst Swapnil Babele.

Oil flows at stake

Azerbaijan currently exports more than 80% of domestic oil production through the BTC pipeline, with output from the ACG fields representing the lion’s share. The Light Azeri crude is transported through Georgia and onward to the Port of Ceyhan in Turkey, and from there to European markets via the Mediterranean Sea.

[contextly_sidebar id=”u8Yr2JQ8nNmCGxTBgYVweErvNJP5TJNl”]

Small volumes of Azeri oil are also exported via two other pipelines. The Baku-Suspa pipeline, operated by BP and with a capacity of 150,000 bpd, is used mainly to export oil from coastal offshore deposits. It starts at the Sangachal terminal near Baku and runs to the Suspa terminal near the Georgian coast, where oil is then shipped to European markets through the Bosphorus Strait in Turkey.

Then there is the Baku-Novorossiysk pipeline, which carries oil from onshore fields operated by Azeri state energy company Socar for export to the Russian Black Sea port of Novorossiysk. The transmission capacity of this pipeline is 100,000 bpd.

Azerbaijan could increase flows through the Baku-Suspa and Baku-Novorossiysk oil pipelines, but this workaround could only compensate for half of the exports that normally flow through BTC.

Some crude volumes are also exported via rail from Azerbaijan to the Batumi and Kulevi terminals, located on Georgia’s Black Sea coast.

Gas flows at stake

In the past couple of years, Azerbaijan has become an important gas exporter for the region, making use of three main arteries in the southern gas corridor. The aforementioned SCP line, which opened in 2006, is 692 km long (443 km in Azeri territory and 249 km in Georgia). When the link is established with the Trans Adriatic Pipeline at the border between Turkey and Greece, the door will open for delivery of Azeri gas to southern Italy. The TAP pipeline, which traverses Greece and Albania before stretching across the Adriatic to Italy, can also allow gas to be diverted to southeastern Europe. Gas exports from Azerbaijan via the Southern Gas Corridor will enable Italy to become a regional gas hub and will provide security of supply to countries currently heavily dependent on gas imports from eastern Europe, mainly Russia.

Any damage to the SCP pipeline relating to the conflict in Nagorno-Karabakh could delay the launch of the TAP pipeline while also disrupting gas deliveries to Turkey. Countries that currently rely on Azeri gas may have to look to Russian gas and new LNG imports in the interim. Turkey probably has the most to lose since it has reduced its imports of Russian gas in favor of Azeri gas and US LNG.

Turkey imported about 24 billion cubic meters (Bcm) of Russian gas in 2018 but these volumes fell to about 15.5 Bcm in 2019 and are expected to fall further in 2020. Turkey has been taking advantage of low spot prices this year and has increased its LNG cargo purchases from the US as well as its imports of pipeline gas from Azerbaijan, which reached about 6.5 Bcm from January to July this year.

Natural gas production in Azerbaijan is currently expected to reach an interim peak in 2022, at which point the natural decline from its mature fields will cause a reduction in pipeline exports. The decline could be reversed again after 2026 if recent Azeri gas discoveries are developed.