(WO) – Despite the accelerating energy transition, oil and gas will remain central to the global energy mix for the foreseeable future as the key hydrocarbon sources continue to satisfy global primary energy demand, which is projected to exceed 650 exajoules (EJ) in the coming years.

Rystad Energy estimates that by 2030, more than 75% of total demand will be met by oil and gas, with emissions climbing as a result. A significant portion of these emissions will originate from upstream activities, particularly hydrocarbon extraction and gas flaring.

Approximately three-quarters of these emissions will be linked to the hydrocarbon extraction process, while the remaining quarter will result from gas flaring. This is expected to contribute around 1.1 billion tonnes of carbon dioxide equivalent (CO2e) annually over the next few years.

This underscores the continuing importance of hydrocarbons, while also highlighting the need for oil and gas companies to build sustainable portfolios and reduce their Scope 1 and Scope 2 emissions to meet medium and long-term targets.

As upstream organizations work to transform into integrated energy players and decarbonize their operations, it is crucial not only to achieve transition goals but also to minimize the carbon footprint of upstream activities, with extraction of these resources accounting for more than 800 million tonnes of CO2e every year.

As investors and governments intensify their focus on carbon-reduction goals, identifying basins that can help lower the overall emissions impact is becoming increasingly important.

Premium energy basins (PEB)—a term coined by Rystad Energy —are particularly valuable because they are rich in oil and gas reserves and offer potential for integrating low-carbon energy sources.

As such, they provide an ideal platform for addressing emission challenges by combining substantial hydrocarbon volumes with opportunities for incorporating low-carbon solutions to reduce overall emissions.

Palzor Shenga, Vice President of Upstream Research at Rystad Energy, said, “A select few basins hold the potential for upstream players to decarbonize while continuing to meet oil and gas demand.”

However, the race to decarbonize hinges on three crucial factors, according to Shenga:

- Accelerating investment

- Overcoming geographical challenges

- Modifying existing infrastructure.

“These changes are essential for unlocking the full potential of these basins and for upstream players to achieve their decarbonization targets,” Shenga concluded.

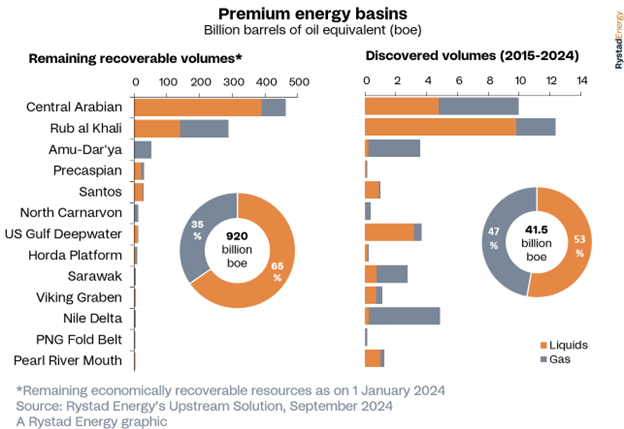

Having analyzed PEBs based on their availability of remaining hydrocarbon resources, development cost, emissions and the availability of new energy sources such as wind and solar, together with their suitability for carbon storage, the Central Arabian and Rub Al Khali basins stand out as carbon-efficient, resource-rich basins with significant potential.

These Middle Eastern basins are at the forefront of PEBs and play a pivotal role in global conventional discovered volumes, especially as global discoveries decline and exploration activity peaks. Separately, these basins also score highly in terms of renewable potential, with both offering more than 6.2 gigawatts (GW) combined of installed and upcoming solar capacity.

Since 2015, these basins have contributed approximately 40 Bbbl in newly discovered volumes, evenly divided between liquids and gas. Egypt’s Nile Delta, driven by Eni’s giant Zohr gas discovery in the Mediterranean Sea, ranks third with about 5 Bboe discovered during this period, followed by the U.S. Gulf Deepwater (3.7Boe) and the Central Asian Amu-Darya (3.6 Bboe) basins.

With combined capital expenditure of $638 billion, the Rub Al Khali, U.S. Gulf Deepwater and Central Arabian basins have seen the highest greenfield investments since 2000. Due to the vast volumes discovered, the unit cost of development in the two Middle Eastern basins has been under $2 per boe.

In contrast, the smaller average resource size in the exclusively offshore U.S. Gulf Deepwater basin has driven development costs to over $9 per boe, with only the Viking Graben basin ($11 per boe) in Northwest Europe having a higher development cost. Significant investments have also been made in resource development in Brazil’s Santos basin ($153 billion) and Australia’s North Carnarvon basin ($140 billion).

Several PEBs offer significant potential for carbon storage, particularly in late-life or abandoned oil and gas fields, which are suitable for enhanced oil recovery or permanent storage.

These basins are increasingly being utilized for carbon capture and storage due to their geological properties. Deep-seated saline aquifers are especially promising, with the U.S. Gulf Deepwater basin leading the way among PEBs in CO2 storage potential, boasting 750 gigatonnes of saline aquifer capacity.