As energy sector demand roars back and commodities market pundits talk about the return of $100 oil, there are new factors in the energy sector pushing producers to extract less — from greater fiscal discipline in the U.S. shale after a decade-long bust to ESG pressure and the ways in which energy executives are being paid by shareholders.

In 2018, Royal Dutch Shell became the first oil major to link ESG to executive pay, earmarking 10% of long-term incentive plans (LTIP) to reducing carbon emissions. BP followed suit, using ESG measures in both its annual bonus and its LTIP. While the European majors were first, Chevron and Marathon Oil are among the U.S. -based oil companies that have added greenhouse gas emissions targets to executive compensation plans.

The oil and gas companies are joining dozens of public corporations across all sectors — including Apple, Clorox, PepsiCo and Starbucks — that tie ESG to executive pay. Last week, industrial Caterpillar created the position of chief sustainability & strategy officer last and said it will now tie a portion of executive compensation to ESG.

As of last year, 51% of S&P 500 companies used some form of ESG metrics in their executive compensation plans, according to a report from Willis Towers Watson. Half of companies include ESG in annual bonus or incentive plans, while only 4% use it in long-term incentive plans (LTIP). A similar report from PricewaterhouseCoopers (PwC) found that 45% of FTSE 100 firms had an ESG target in the annual bonus, LTIP or both.

“We will continue to see the percentage of companies [linking ESG to pay] increase,” said Ken Kuk, senior director of talent and rewards at Willis Towers Watson. And although right now more than 95% of instances of ESG metrics are in annual bonuses, “there is a shift more toward long-term incentives,” he said.

A related survey by the firm last year, of board members and senior executives, revealed that nearly four in five respondents (78%) are planning to change how they use ESG with their executive incentive plans over the next three years. This reflects the current purpose-over-profit debate in the corporate world, with the environment ranking as the top priority.

Pressuring the fossil fuel industry

In 2020, petroleum accounted for about a third of U.S. energy consumption, but was the source of 45% of the total energy-related CO2 emissions, according to the U.S. Energy Information Administration. Natural gas also provided about a third of the nation’s energy and produced 36% of CO2 emissions. Oil and gas companies have largely abandoned coal, which accounted for about 10% of energy use and accounted for nearly 19% of emissions.

Investors are increasingly focused on ESG, and more have been pressuring the fossil fuel industry to shrink its global carbon footprint and the associated risks to operations and bottom lines. “The increase in momentum that the investment community has put around ESG is driving the discussion into climate [change],” said Phillippa O’Connor, a London-based partner at PwC and a specialist in executive pay. “We can’t underestimate the impact that investors will continue to have for the next couple of years.”

Investor input played a decisive role in Shell’s seminal decision, as well as those at competitors that followed suit. And while executive compensation wasn’t high on the docket at Exxon Mobil’s shareholder meeting last spring, the industry was gobsmacked when the climate-activist hedge fund Engine No. 1 won three seats on its board of directors. The coup, as it was roundly described, may ultimately deemphasize Exxon’s reliance on carbon-based businesses and move it more toward investments in solar, wind and other renewable energy sources — and in the process lead to ESG-linked pay packages.

“We look forward to working with all of our directors to build on the progress we’ve made to grow long-term shareholder value and succeed in a lower-carbon future,” Exxon chairman and CEO Darren Woods said in a statement shortly after the proxy vote.

Meanwhile, financial regulators also are eyeing climate change as a factor for investors to consider. The Securities and Exchange Commission has indicated that ESG disclosure regulation will be a central focus under new Chair Gary Gensler, from climate to other ESG factors such as labor conditions.

There’s nothing novel about incentivizing corporate leaders to hit predetermined targets, particularly for increasing revenue, profits and shareholder returns by certain increments. Oil and gas companies, because of their hazardous extraction operations — from underground fracking wells to offshore drilling rigs — have for years established incentives for improving workplace safety.

Following the Enron accounting and fraud scandal in 2001, meeting new governance mandates (Sarbanes-Oxley Act) was the basis for rewards. Then came added remuneration for achieving internal goals set for quality, health and wellness, recycling, energy conservation and community service — wrapped into corporate social responsibility. Sustainability then became the catch-all for establishing executive performance metrics around environmental stewardship, diversity, equity and inclusion (DEI) in the workplace and ethical business practices — all of which now reside under the ESG umbrella.

ESG is tricky, and existing carbon targets have critics

Although the trend is expected to continue, experts warn that the process can be tricky, and targets designed by oil and gas companies to combat climate already have critics.

Including emission-reduction targets in executive pay packages may compel oil and gas companies to walk their public-relations talk about being good corporate citizens. Yet the methodology can be challenging. “It’s not the what, but the how,” said Christyan Malek, an industry analyst at JP Morgan. For example, a company can state how much is has lowered its global carbon emissions in a given year. “But that’s very limited,” he said, “because they’re not disclosing their emissions by region,” which can widely vary from one location to the next. “When it comes to carbon intensity, it’s in the [overall] portfolio.”

Or a company can ply in greenwashing through carbon offsets. “I have massive emissions, so I’ll [plant] a bunch of forests, and that way I neutralize myself,” Malek said — while the company is still producing the same amount of emissions. “You’re disclosing in a way that’s better optically than it is in reality. Disclosure has to work hand in hand with compensation.”

The optics of oil and gas companies paying well for doing good might help the industry’s image among a general public increasingly concerned about the calamitous impacts of human-induced climate change, exacerbated by the latest, and most dire, related U.N. report and a string of deadly floods, hurricanes, heatwaves and wildfires. But experts focused on climate and the energy sector note that sector targets often don’t go far enough, related to reducing intensity of fossil fuel operations, not underlying production of fossil fuels, and dealing only with Scope 1 and Scope 2 emissions, not the Scope 3 emissions which are the largest share of the climate problem.

O’Connor said that companies should be careful how they align ESG metrics with incentives. “ESG is a broad and complex set of metrics and expectations,” she said. “That’s one of the reasons why we’re seeing a number of companies use multiple metrics rather than a single measure, to get a better balance of considerations and perspectives across the ESG forum. There isn’t a one-size-fits-all policy in this, and there’s a danger in trying to move too quickly and revert to some kind of standard.”

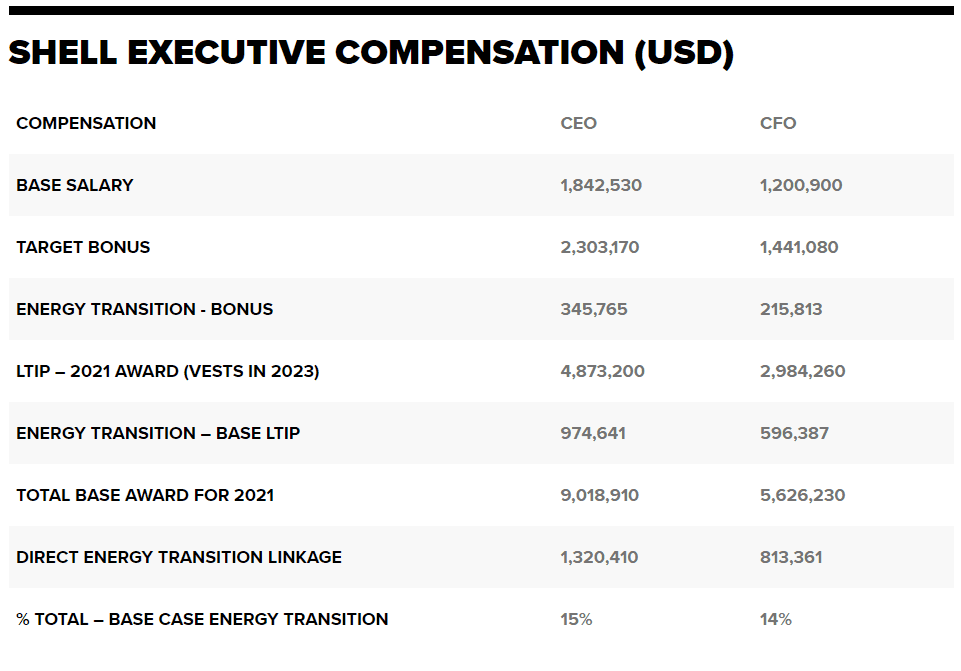

The pandemic placed an unexpected hard top on compensation incentives in 2020, and with the global economy decimated last year, Shell’s remuneration board decided to forego bonuses for CEO Ben van Beurden, CFO Jessica Uhl and other top executives, and there was no direct link in their LTIPs to delivery of energy transition targets.

The energy sector has roared back this year amid strong global economic growth and demand for oil and gas amid lower supply has led to a spike in prices. That could incentivize oil and gas companies to produce more, but at the same time, compensation to to energy transition targets ae going up. At Shell, the 2021 annual bonus is targeted at 120% of base salary for the CEO and CFO, which remain the same as set in 2020, at $1,842,530 and $1,200,900, respectively. Within this, though, progress in energy transition is now up from 10% to 15% of the total amount that can be awarded. In addition, energy transition is part of the LTIP which vests three years in the future, based on Shell’s 2020 annual report.

The deleterious role that carbon emissions play in climate change will continue to put pressure on oil and gas companies to embrace the International Energy Agency’s goal of achieving net-zero by 2050. Beyond complying with regulatory mandates, though, linking reduction targets to executives’ compensation may be a critical driver in affecting change.

[contextly_sidebar id=”DiamjoY7uGZau1bhXJ37kAqiqS3bWj5Y”]