An Exclusive Interview with Garth Braun, Chairman, President and CEO of Blackbird

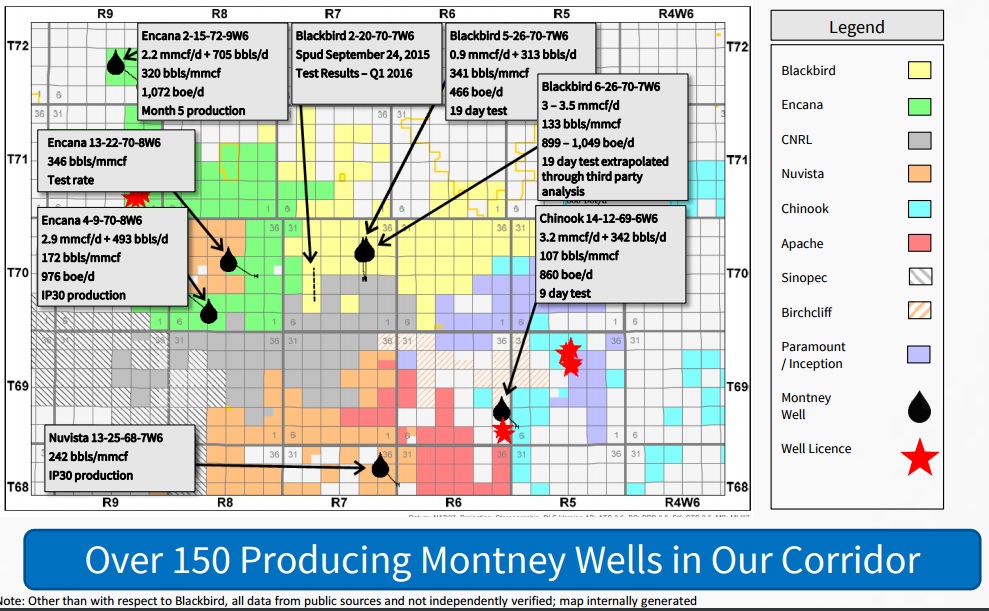

Blackbird Energy (ticker: BBI, www.blackbirdenergyinc.com) is in the early stages of developing its 75 sections (48,000 acres) of the Montney fairway in Alberta, but results from its 2-20-70-7W6 well indicate there may be plenty of running room ahead.

In a company release issued on January 28, 2016, Blackbird announced the 2-20 produced 1,768 BOEPD (36% liquids) in a 24-hour test, beating its gas and BOE type curves by 109% and 80%, respectively. Since the production was derived from an outpost well, BBI management says future wells have the potential for even greater returns with reduced expenditures.

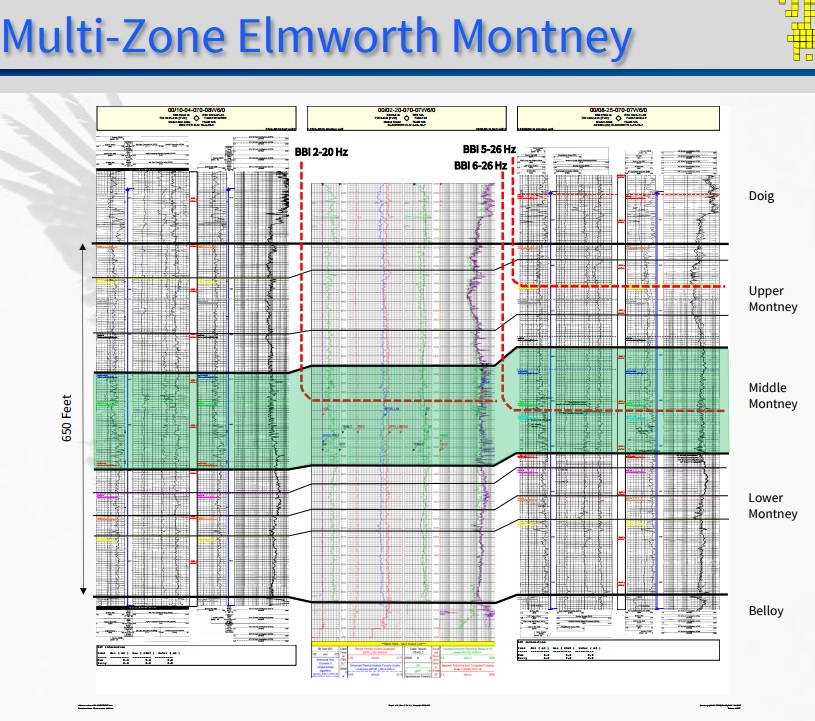

“However, this is much more important than the BOE,” said Garth Braun, Chairman, President and CEO of Blackbird, in an interview with Oil & Gas 360®. “We believe it demonstrates the productivity of the Middle Montney throughout a minimum of 25 sections of our land. We’ve established the deliverability and the liquids component of the area, and with the near proximity drilling that was completed by Encana Corp. (ticker: ECA, www.encana.com) just to the west, we believe Blackbird has three distinct Montney intervals throughout those 25 sections.”

BBI management believes its delineated acreage holds four drilling locations per interval. With three intervals per section, that amounts to 12 wells per section and 300 wells total for its 25 delineated sections, which accounts for about one-third of Blackbird’s position. Braun believes future wells can be completed at costs of $7.25 million apiece with the slickwater method, down from $7.70 million associated with the 2-20. “These wells are economic in the current environment,” he said.

Click here for the company’s updated presentation, incorporating the news from today’s announcement.

The Neighbors: Encana

Blackbird’s operating position is surrounded by some of the biggest names in the business, including Encana, Apache Corp. (ticker: APA, www.apache.com) and Canadian Natural Resources (ticker: CNQ, www.cnrl.com). Encana has an active drilling program, and the large-cap producer holds the area in high regard: it is one of four core areas in North America, garnering attention with the likes of the Eagle Ford and Permian plays on the United States.

The Montney’s hydrocarbon characteristics are similar to that of the Eagle Ford Shale, highlighted by specific sweet spots and transitions from dry gas to liquids rich/free condensate regions. Encana’s progress on the region powered Blackbird’s decision to officially list its 25 sections as a delineated area.

One of those wells is ECA’s 2-15-72-9W6, which Braun says has returned more 186 MBOE of condensate and 750 MMcf in 11 months.

Technology is the Name of the Game

Of course, capital efficiency is paramount in the current commodity downturn, and some of the capital is derived directly from technological advents designed to give operators the best bang for the buck. Yesterday, Stephens Inc. released an in-depth review on how the most technologically advanced oilservice companies provide the greatest upside in the investment arena.

“When we attended The Oil & Gas Conference® 20 last August, operators in the Marcellus and Permian spoke continuously about innovation in production,” Braun said. “The same goes with the Montney – it’s a very technical formation to work in.”

Blackbird is leading the pack among innovations in the play, as the Calgary-based E&P was the first to drill a monobore in the corridor and then executed the longest sliding sleeve completion in the fairway. As its knowledge of the play increased, BBI elected to use individual completions per interval via the sliding sleeve method as opposed to plug-n-perf clusters, shortening the interval length in the process. Finally, BBI finalized Canada’s largest-ever CO2 completion on the 2-20 with the intention of generating greater reservoir visibility. With such innovations in its drilling program, Blackbird management believes the 2-20 can be a repeatable, consistent example of its future wells.

Blackbird’s Next Chapter

Blackbird’s Next Chapter

Intervals that will be exploited in the future include the Upper Montney/Lower Doig region – a current target of Encana’s drilling program. The Lower Montney is also on the radar and was the focus of a recent test with Schlumberger (ticker: SLB, www.slb.com).

“We drilled and logged a pilot well and it shows plenty of resource potential, we just don’t believe we should be focusing our completions on the region at this time,” said Braun. “We’d like to have more industry leadership before we get into that zone. We believe it’s very gassy, we just don’t know the liquids cut.”

Going forward, BBI management expects 70% of its drilling program to target the Upper Montney, with the remaining 30% exploiting the lower region. The company owns full working interest across its acreage, which can be further exploited once the company executes on its impending infrastructure buildout. BBI expects agreements to be finalized within the next 90 days.

The company had $23 million in working capital and no debt prior to drilling the 2-20, and plans on maintaining a very cost-effective balance sheet throughout the course of 2016.

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.